Debt poses a growing threat to the financial security of many Americans—and not just college graduates with exorbitant student loans. Recent studies by the Center for Retirement Research at Boston College (CRR) and the Employee Benefit Research Institute (EBRI) reveal an alarming trend: The percentage of older Americans with debt is at its highest level in almost 30 years, and the amount and types of debt are on the rise.

Debt Profile of Older Americans

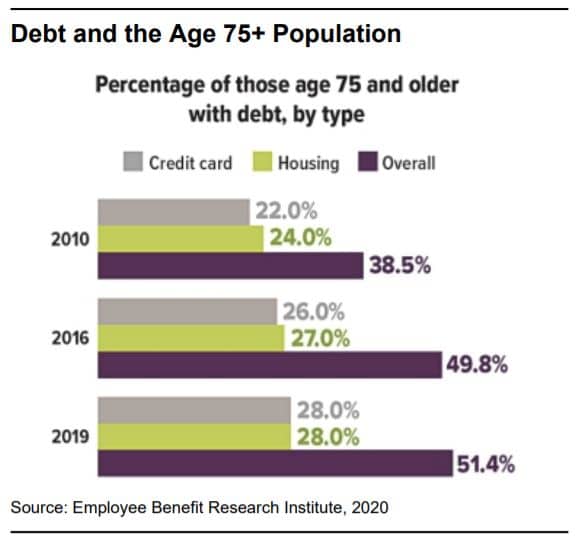

In the 20-year period from 1998 to 2019, debt increased steadily for families with household heads age 55 and older; in recent years, however, the increase has largely been driven by families with household heads age 75 and older. From 2010 to 2019, the percentage of this older group who carried debt rose from 38.5% to 51.4%, the highest level since 1992. By contrast, the percentage of younger age groups carrying debt either rose slightly or held steady during that period.

Mortgages comprise the largest proportion of debt carried by older Americans, representing 80% of the total burden. According to EBRI, the median housing debt held by those age 75 and older jumped from $61,000 in 2010 to $82,000 in 2019. The CRR study reported that baby boomers tend to have bigger debt loads than older generations, largely because of pricey home purchases financed by small down payments.

Consequently, economic factors that affect the housing market—such as changes in interest rates, home prices, and tax changes related to mortgages—may have a significant impact on the financial situations of both current and future retirees.

Credit-card debt is the largest form of non-housing debt among older Americans. In 2019, the incidence of those age 75 and older reporting credit-card debt reached 28%, its highest level ever. The median amount owed rose from $2,100 in 2010 to $2,700 in 2019.

Medical debt is also a problem and often the result of an unexpected emergency. In the CRR study, 21% of baby boomers reported having medical debt, with a median balance of $1,200. Among those coping with a chronic illness, one in six said they carry debt due to the high cost of prescription medications.

Finally and perhaps most surprisingly, student loan obligations are the fastest-growing kind of debt held by older adults. Sadly, it appears that older folks are generally not borrowing to pursue their own academic or professional enrichment, but instead to help children and grandchildren pay for college.

How Debt Might Affect Retirement

Both the CRR and EBRI studies warn that increasing debt levels may be unsustainable for current and future retirees. For example, because the stress endured by those who carry high debt loads often results in negative health consequences, which then result in even more financial need, the effect can be a perpetual downward spiral. Another potential impact is that individuals may find themselves postponing retirement simply to stay current on their debt payments. Yet another is the risk that both workers and retirees may be forced to tap their retirement savings accounts earlier than anticipated to cope with a debt-related crisis.

If you are retired or nearing retirement, one step you can take is to evaluate your debt-to-income and debt-to-assets ratios, with the goal of reducing them over time. If you still have many years ahead of you until retirement, consider making debt reduction as high a priority as building your retirement nest egg.

If you have questions or need assistance, contact the Experts at Henssler Financial:

- Experts Request Form

- Email: experts@henssler.com

- Phone: 770-429-9166

Sources: Center for Retirement Research at Boston College, 2020; Employee Benefit Research Institute, 2020

Disclosures: The following information is reprinted with permission from Forefield, a division of Broadridge Financial Solutions, Inc. The investments referenced within this article may currently be traded by Henssler Financial. All material presented is compiled from sources believed to be reliable and current, but accuracy cannot be guaranteed. The contents are intended for general information purposes only. Information provided should not be the sole basis in making any decisions and is not intended to replace the advice of a qualified professional, such as a tax consultant, insurance adviser or attorney. Although this material is designed to provide accurate and authoritative information with respect to the subject matter, it may not apply in all situations. Readers are urged to consult with their adviser concerning specific situations and questions. This is not to be construed as an offer to buy or sell any financial instruments. It is not our intention to state, indicate or imply in any manner that current or past results are indicative of future profitability or expectations. As with all investments, there are associated inherent risks. Please obtain and review all financial material carefully before investing. Henssler is not licensed to offer or sell insurance products, and this overview is not to be construed as an offer to purchase any insurance products.